Wind and solar capacity in south-east Asia climbs 20% in just one year, report finds

Solar and wind capacity in the Association of Southeast Asian Nations (ASEAN) region increased by 20% in 2023, bringing the total to more than 28 gigawatts (GW).

The technologies now make up 9% of electricity generating capacity in ASEAN countries – Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand and Vietnam – according to a new report from Global Energy Monitor (GEM).

Combined with a large base of hydropower, the growth in wind and solar takes the bloc close to its renewable energy capacity target of 35% by 2025, GEM says.

Building an additional 17GW of utility-scale solar and wind projects in the next two years – those that feed power directly into the electricity grid – would be sufficient to reach the goal, it adds.

In fact, it says the region is on track to sail past its target, nearly doubling wind and solar capacity in the next two years by adding a further 23GW of new projects

An even larger 220GW pipeline of new utility-scale wind and solar capacity has been announced, or entered pre-construction or construction stages, according to GEM’s analysis, though only 6GW of this is currently being built.

However, ASEAN countries collectively have one of the fastest-growing economies in the world and have seen very rapid recent electricity demand growth of 22% per year between 2015 and 2021. This has translated into continued support for gas and coal power in the region, even though demand growth is expected to slow.

While renewables have the potential to temper the growth in fossil fuel demand, wind and solar expansion face regulatory hurdles and a lack of supportive policy, GEM adds.

Success so far

ASEAN added 3GW of solar capacity in 2023, increasing installed capacity by 17% over 2022 levels, according to GEM’s report.

Despite solar seeing a larger overall capacity increase, operational wind capacity saw a larger comparative rise, growing by 29%, or 2GW, since January 2023.

Offshore wind now accounts for 2GW of the operating 9GW of utility-scale wind capacity in the region.

Given the technical challenges and associated higher costs of offshore wind, this is particularly noteworthy, GEM states.

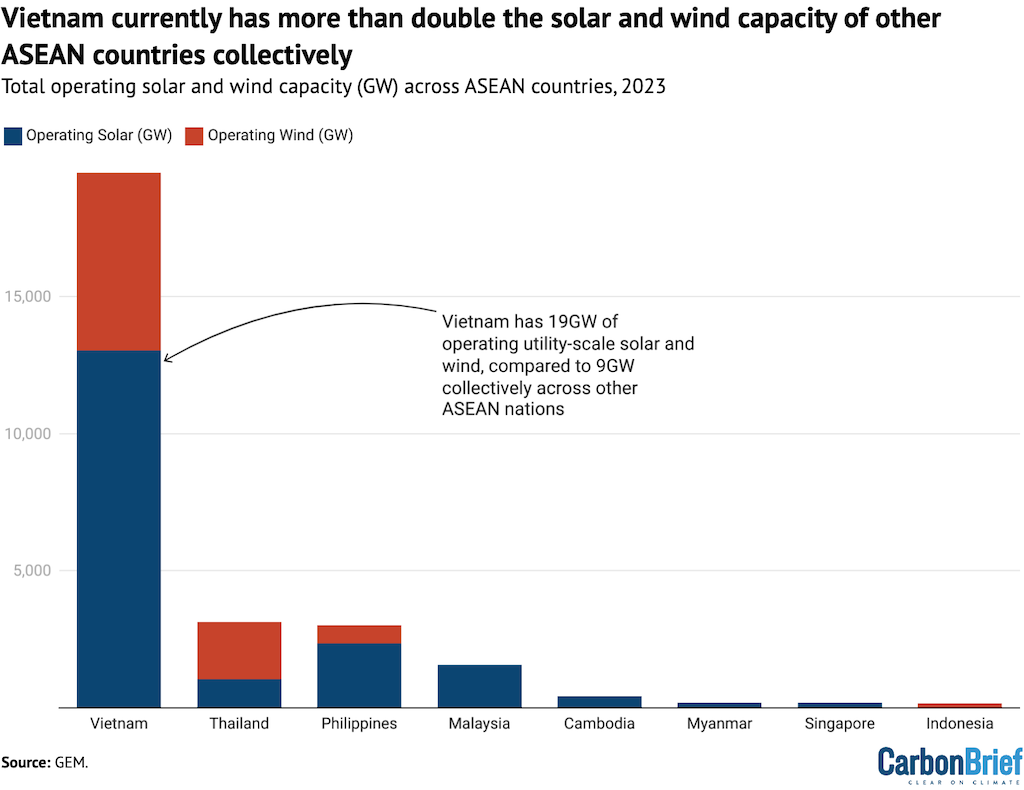

Vietnam has by far the most utility-scale solar and wind capacity of all the ASEAN nations, as seen in the chart below.

The increase in utility-scale solar and wind capacity over the past year has come as a result of a supportive policy environment across many countries in the ASEAN region, says GEM.

In 2017, Vietnam deployed a series of investment policies designed to bring utility scale-solar projects into operation, for example. Two feed-in-tariff (FiT) programs were deployed by the country’s state-owned utility between 2017 and 2020.

However, when these programs expired, Vietnam failed to administer a replacement, GEM says. As such, despite the nation adding 12GW of utility-scale solar capacity between 2019 and 2021, gaps in energy policy have started to limit progress.

Just 1GW of utility-scale solar and wind was commissioned in Vietnam in 2022, in comparison with nearly 4GW in 2021.

Thailand and the Philippines currently have the second and third highest utility-scale solar and wind capacity in the region, with 3GW of operating capacity each.

Thailand is the second largest economy in ASEAN after Indonesia and has benefitted from being seen as a “low-risk country”, notes GEM, with few barriers for investment.

The Philippines, meanwhile, hosts a “streamlined project bidding system”, which allows for an “unencumbered pipeline of project development”, GEM says. Currently, around three-quarters of its operational utility-scale solar and wind capacity comes from solar.

Future growth

There is currently a total of 222GW of announced, pre-construction and construction-stage utility-scale wind and solar capacity in ASEAN countries, according to GEM’s research.

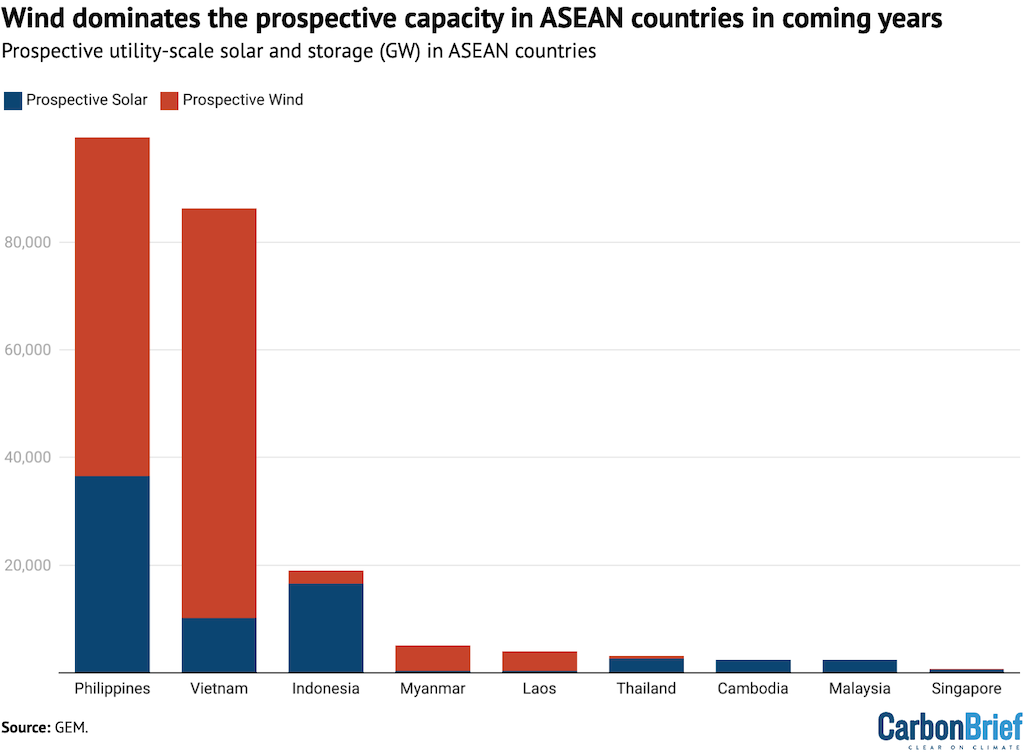

More than 185GW of this pipeline of projects is in the Philippines and Vietnam, meaning they account for more than 80% of prospective capacity in the region. This is shown in the figure below.

More than 60% of the pipeline in Vietnam and the Philippines comes from planned offshore wind development, GEM says, of 72GW and 52GW respectively.

The Philippines is responsible for 45% of prospective capacity in ASEAN countries. Its Green Energy Auction Program (GEAP) aims to facilitate the development of more than 11GW of renewable energy.

In March 2023, it held an auction securing just over 300 bids to develop 3GW of solar, onshore wind and bioenergy with 2024–2026 start dates.

This capacity fell short of the level targeted, but represented a 75% increase on the amount secured in 2022’s auction, notes GEM.

Offshore wind comprises 52% of the Philippines’ prospective utility-scale renewable capacity, with five times more offshore wind than onshore.

In April 2023, the nation issued an executive order, outlining cooperation between private investors and the government on offshore wind. Since then, offshore wind contracts have more than doubled to nearly 80, representing 61GW of capacity, GEM notes.

Vietnam has more than 86GW of prospective capacity, including 72GW of offshore wind. However, just 2% is currently being built, due in part to the country’s “lack of concise and reliable renewable energy policies that could serve as a crucial roadmap for project implementation”, states GEM.

A further 40GW of utility-scale solar and wind projects in Vietnam are considered by GEM to be “shelved”, because they have seen no progression or announcements in the past two years.

Vietnam is working on a just energy transition partnership (JETP) with a group of developed countries. It also released its latest national electricity development plan for 2021–2030, also known as the power development plan 8 (PDP8).

The alignment of these policies and funding schemes is still in development, and therefore their impact cannot yet be determined, notes GEM.

Laos is aiming to “punch above its economic weight” in the development of utility-scale solar and wind capacity, GEM says. At more than 3GW, its prospective capacity rivals that of Thailand, despite the country’s economy being only 2% of the size.

Laos’ prospective utility-scale solar and wind capacity surpasses that of Malaysia by more than 150%, despite having an economy that is more than thirty times smaller. This ambition is being driven by financial collaboration with ASEAN partners, according to GEM.

Laos is set to house the region’s largest onshore windfarm. Monsoon windfarm is currently under construction and expected to have a capacity of 600 megawatts (MW) when complete.

Despite this large pipeline of ASEAN wind and solar projects, however, only 6.3GW (3%) is currently under construction, notes GEM.

Reaching renewable ambitions

The target for renewables to make up 35% of electricity generating capacity by 2025 is “easily attainable and ultimately unambitious for ASEAN”, according to GEM.

Renewables already make up 32% of electricity capacity in ASEAN countries, GEM says, meaning the 35% target can be met easily.

Moreover, while annual growth in electricity consumption is expected to slow from the annual 22% since 2014 to just 3% a year out to 2030, GEM says rising demand will continue to drive expansion in fossil fuel power infrastructure in the region.

Hitting the 35% target would only require ASEAN countries to commission 17GW of new renewable capacity by 2025, GEM says, of which 6.3GW is already under construction.

Yet there is in excess of 220GW of prospective utility-scale solar and wind in development, with a total of 23GW set to be operational by 2025.

This means the region is on track to beat its target and nearly double its installed wind and solar capacity in just two years, according to GEM, with scope to go even further and reduce the need for fossil fuel expansion.

For now, fossil fuels remain entrenched in the region, restricting new investment in utility-scale wind and solar, GEM states.

Gas and coal each account for approximately 30% of ASEAN countries’ total installed capacity, and coal-fired power capacity has seen an annual growth rate of 7% since 2017.

With electricity demand growth currently outpacing the rollout of renewable energy capacity, gas and coal are expected to continue to grow in coming years, GEM says.

National energy policies have touted the use of gas as a “stepping stone” in the energy transition and ASEAN countries are likely to be net importers of gas by 2025.

Insufficient grid infrastructure investment is also a “persistent hurdle” for integrating utility-scale solar and wind, notes GEM.

As such, while there is a clear effort being made to ramp up renewable energy, this continues to be complicated by a buildout of fossil fuels and low solar and wind construction rates, concludes GEM. The report adds:

“By doubling down on bringing as much of the 220GW of prospective utility-scale solar and wind projects into fruition, ASEAN countries will be poised to not only meet regional renewable energy targets, but pave the way to transition from fossil fuels.”

Sharelines from this story